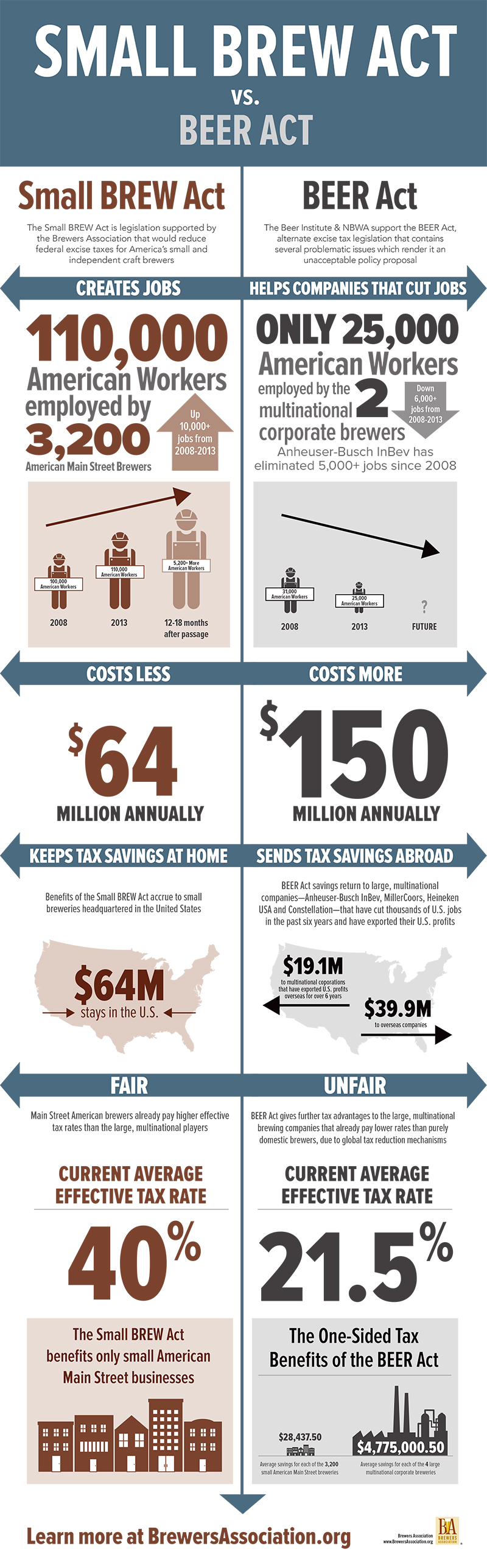

Small BREW Act vs. Fair BEER Act

This year, two competing beer excise tax reform bills reside in Congress: the Small Brewer Reinvestment and Expanding Workforce (BREW) Act (S 375 / HR 232) and the Fair Brewers Excise and Economic Relief (BEER) Act (HR 767). Currently, about 40 percent of a beer’s cost goes to the taxes, including excise, sales and business taxes. Both acts would reform the excise tax in a graduated scale to benefit brewers. But the scale itself and other details of the bills differ from there.

The Brewers Association supports the Small BREW Act, which it feels does a better job of supporting smaller craft brewers rather than macrobrewers. This bill proposes that the tax rate on a brewery’s first 60,000 barrels should be reduced to $3.50 per barrel from the current $7. From 60,001 to 2 million barrels, the tax rate should be $16 per barrel instead of $18. After 2 million barrels, the tax rate would be the current $18-per-barrel rate.

Also, the act would raise the cap of what is considered a small brewer from one that produces 2 million barrels per year to one that produces 6 million, and only breweries under the 6 million barrel maximum would qualify for the tax reform. For some perspective, MillerCoors makes more than 6 million barrels at just one of its many North American facilities each year, and it is the second-largest brewer in the U.S. behind Anheuser-Busch InBev (AB InBev).

More than just saving money for the craft beer industry, the Brewers Association sees this bill as an opportunity for job growth in the United States.

“We believe the impact is by and large that small brewery owners can take that money, reinvest it into their brewery infrastructure and produce more beer,” says Bob Pease, CEO of the Brewers Association. “And when small brewers produce more beer, they create more jobs and hire more workers. We’ve always positioned [the Small BREW Act] as a job creations bill.”

The Beer Institute, on the other hand, supports the Fair BEER Act, which it feels better helps craft brewers. The institute also wants to benefit brewers across the board, as it has no cap or maximum barrelage brewers can produce to benefit from the tax reform. With this bill, for the first 7,143 barrels, brewers would pay no excise tax. That number came from the current level declared by the Alcohol and Tobacco Tax and Trade Bureau for paperwork and tax payment purposes.

For 7,144 to 60,000 barrels, the tax rate would be $3.50 per barrel, and for 60,001 to 2 million barrels, the tax rate would be $16 per barrel. After 2 million barrels, the tax rate would be the current $18 per barrel. From 7,144 barrels and above, the two acts are actually in agreement.

“We’ve designed our bill to give tax relief to small brewers in particular,” says Jim McGreevy, president and CEO of Beer Institute. “We think it brings complete relief to small brewers underneath that threshold, particularly the many, many thousands that are out there who brew 7,143 barrels and under.”

Where the Two Bills Differ

While the Small BREW Act limits the barrels a brewer can produce to qualify for the proposed tax rate, the Fair BEER Act would apply to all brewers, including industry giants like AB InBev and MillerCoors. According to an infographic from the Brewers Association, these two bills could have widely differing impacts on everything from beer industry jobs to the cost of the tax rate cuts.

{kind=link}

Another major difference is the definition of a small brewer, which the Brewers Association wants to change to 6 million. The Beer Institute, however, says that thousands of breweries have opened in the past decade with the 2 million level in place and thus sees no need to change it.

The National Beer Wholesalers Association (NBWA) also has reservations about the definition change.

“We’re concerned that the legislation could change the industry structure by creating a new, unrealistic definition of a small brewer,” says Craig Purser, president and CEO of the NBWA. “… If Congress wishes to reform excise taxes for brewers, it should do so in a way that reflects current government and industry classifications.”

Finally, the Fair BEER Act accounts for importers, while the Small BREW Act does not. The Small BREW Act wants to solely support American jobs and small breweries, but because the Fair BEER Act would cover all players in the beer industry, it includes importers as well. The Beer Institute has concerns about a trade challenge if tax reform does not include importers.

How the Bills Come Together

It is possible that either bill could mean breweries pass savings down to customers, but neither bill offers any definite promise of lower prices. However, because brewers would likely reinvest the saved tax dollars into their businesses, consumers could see more volume and diversity of beer if either bill passes.

Pease believes either bill would need a broader legislative vehicle to pass it. This would likely be some sort of comprehensive tax reform.

Another issue is that the competing bills could mean a split in congressional co-sponsors, which may leave both bills without enough support to pass.

“Brewers won’t get relief unless there is one bill,” McGreevy says. “It’s better for industries to speak with one voice.”

Both organizations agree that these bills affect how Congress perceives the beer industry and that the bills “tell the story of American craft brewing in Congress,” Pease says.

“It’s impossible to know what impact either the BREW or BEER Act would have ultimately,” McGreevy says. “It’s important that we’re having the discussion to determine what the excise tax should be going forward for both large and small. … There’s a lot of support for beer up on Capitol Hill, and I think we should take advantage of it.”